Abstract

This study examines the critical factors driving the adoption and integration of blockchain technology in accounting education. Employing a moderated model based on the technology acceptance model (TAM), the study investigates what motivates faculty members to adopt and integrate blockchain. Organizational support serves as a key moderating factor in this study. The study employed a quantitative approach, analyzing data from 191 faculty members at Indian universities and colleges using SmartPLS 4 software. The findings emphasize the significance of organizational support in shaping behavioral intentions, with notable effects on perceived usefulness and attitudes toward blockchain adoption. Additionally, perceived ease of use indirectly affects behavioral intentions through its impact on perceived usefulness and attitude. The moderated model explained 64% of the variance in behavioral intentions toward blockchain integration in accounting education. These results offer valuable implications for educational policy, not only in India but also in similar developing nations. By comprehending the relationship between organizational support and faculty members’ perceptions, policymakers can formulate strategies to effectively integrate blockchain technology into accounting education, encouraging innovation in university practices for the digital era.

Similar content being viewed by others

Introduction

Blockchain is a cutting-edge accounting technology that has gained significant attention from industry and academia since its introduction (ICAEW, 2018; Dehghani et al. 2022). This technology can potentially streamline transaction and asset accounting processes by offering a comprehensive bookkeeping system (ICAEW, 2018). One of the key benefits of blockchain is its capacity to store data (Sarwar et al. 2021) securely. Implementing blockchain brings several advantages to companies (Kshetri, 2018; Habib et al. 2022): it offers a transparent and unalterable record of all financial transactions, enhancing the accuracy and reliability of financial reporting. Additionally, since multiple network nodes verify each transaction, it reduces the risk of fraud and errors. It also boosts the efficiency of financial reporting by enabling the automatic generation of financial statements using blockchain data. Consequently, rights, obligations, and provenance become clearer, enabling the accounting profession to record more types of activities than ever before (ICAEW, 2018). The benefits of this technology are attracting numerous businesses, and experts anticipate that it will significantly shape the business landscape and society in the coming decades (Javaid et al. 2022; Albayati et al. 2020; Bonsón and Bednárová, 2019).

Although blockchain technology offers promising benefits, its incorporation into accounting education remains underexplored. Critics argue that traditional accounting curricula often struggle to keep pace with technological advancements, potentially compromising the relevance of accounting education in the rapidly changing professional landscape (Qasim and Kharbat, 2020; Al-Hattami, 2021, 2023). As a result, there is a critical need to bridge this gap by integrating blockchain technology into accounting curricula, providing students with the necessary skills for future success (Qasim and Kharbat, 2020; Sledgianowski et al. 2017; Polimeni and Burke, 2021; Singh et al. 2023).

Blockchain is a technology with enduring relevance and a significant impact on the accounting profession. As such, universities must start incorporating blockchain education into their curricula today (Smith, 2017). By integrating blockchain into accounting education, students can gain a deeper understanding of its applications and advantages in accounting. This preparation can help students adapt to the evolving industry and acquire the skills necessary for embracing new technologies (Stern and Reinstein, 2021; Novak et al. 2022; Fernandez and Guat, 2023).

One approach to this integration is introducing blockchain concepts into existing accounting courses such as auditing, financial accounting, and management accounting. Additionally, ready-made educational accounting software that demonstrates blockchain’s mechanics can be employed, as suggested by Al-Hattami (2021, 2023), alongside other foundational tools such as SAP, Motakamel, and Onyx. However, this shift may place additional responsibility on faculty members, who must take on the role of “early adopters” and later share their expertise with peers and students (Smith, 2017).

Academics, including faculty, have a duty to prepare students for the changing landscape of the accounting profession (Al-Hattami, 2023; Trapnell, 2023). According to Moore and Felo (2022), higher education must equip students with the essential skills and competencies needed for success in the workplace. If hiring firms find university graduates competent, then universities can consider themselves successful in meeting industry demand (Kroon and Alves, 2023). Therefore, the key is ensuring compatibility between industry needs and the skills university graduates possess, enabling them to excel in their roles.

Despite growing calls for blockchain technology integration, faculty members’ behavioral intentions toward adopting it in accounting education remain uncertain. To fill this gap, the current study examines Indian university faculty members’ intentions regarding blockchain integration in accounting education. Specifically, the study uses the Technology Acceptance Model (TAM) to evaluate faculty members’ attitudes and perceived usefulness of blockchain adoption, while also investigating how organizational support (OS) influences these intentions.

TAM, developed by Davis (1989), has been widely used to understand the acceptance and adoption of new technologies in various contexts, including education (Granić and Marangunić, 2019; Al-Rahmi et al. 2022; Al-Hattami, 2023; Al-Adwan et al. 2023; Lin and Yu, 2023). This study seeks to provide insights into the factors affecting faculty members’ intentions by applying TAM to blockchain adoption in accounting education.

Furthermore, previous research emphasizes the importance of organizational factors in technology adoption, guiding the exploration of OS’s moderating role (Naujokaitiene et al. 2015; Al-Hattami et al. 2024a, 2024b). Understanding how organizational support affects faculty members’ intentions can illuminate the dynamics of blockchain integration in academic settings.

The research question for this study is: What factors influence faculty members’ behavioral intentions toward adopting and integrating blockchain technology in accounting education, and how does organizational support moderate these intentions?

Since the integration of blockchain technology in accounting education is a relatively new area of research, this study addresses a gap in the existing literature by exploring the specific factors and conditions that influence adoption intentions, particularly in the context of the moderating role of operating systems. Understanding these factors can aid in the design of educational programs that enrich the learning experience, ultimately producing graduates proficient in emerging technologies (Qasim and Kharbat, 2020; Stern and Reinstein, 2021). The study’s findings could have significant policy implications for educational institutions and policymakers. Insights into the factors affecting technology adoption can guide the creation of strategies and policies that support the integration of blockchain in accounting education.

Literature review and hypotheses development

Despite the increasing interest in blockchain technology and its potential applications in accounting, there is limited research on the intention to adopt and integrate blockchain within accounting education. For instance, a PWC (2018) study revealed that 84% of surveyed executives considered blockchain important, yet only 15% had implemented it in their organization. However, this study did not specifically address accounting education.

Kshetri (2018) examined the use of blockchain in supply chain management, emphasizing the need to educate and train accounting professionals to effectively leverage blockchain technology in auditing and accounting. Other research has explored the factors affecting blockchain adoption in supply chain management (e.g., Tasnim et al. 2023; Mukherjee et al. 2023; Al-Swidi et al. 2024).

Similarly, Sciarelli et al. (2022) looked at the factors influencing blockchain adoption in companies, while Albayati et al. (2020) analyzed customer acceptance of cryptocurrency transactions via blockchain. Although these studies identified several influential factors, such as perceived usefulness and ease of use, they did not specifically focus on accounting education.

Qasim and Kharbat (2020) and Singh et al. (2023) examined blockchain usage in accounting and its potential impact on the profession. These studies emphasized the importance of incorporating blockchain into accounting education but did not specifically explore intentions for adopting and integrating blockchain into accounting education.

On the other hand, AlShamsi et al. (2022), in their systematic review, noted that previous studies have largely focused on the adoption of blockchain technology at the organizational level, overlooking the individual perspective. Chen et al. (2018) praised the benefits of blockchain and suggested its use in the education sector to support academic degree management, reduce degree fraud, and evaluate learning outcomes. Other review studies (e.g., Mohammad and Vargas, 2022; Bhaskar et al. 2021; Dash et al. 2022) found that while blockchain has advantages, it still faces challenges, and its acceptance in the education sector remains low. Savelyeva and Park (2022) found that research on blockchain in education primarily addresses its applications in administration, financing, and management, focusing on its technological aspects. No study has examined the intention of adopting and integrating blockchain within accounting education from the perspective of faculty members. Therefore, this study aims to fill that gap.

Based on the TAM, this research hypothesized and tested a moderated model to explore the factors influencing the intention to adopt and integrate blockchain within accounting education. TAM is a widely recognized leading model for explaining behavioral intention as a solid foundation. The study utilized the key variables from TAM—perceived usefulness, perceived ease of use, attitude, and behavioral intention (Davis, 1989; Gado et al. 2022; Ullah et al. 2021; Al-Hattami, 2023; Al-Hattami and Almaqtari, 2023; Al-Adwan et al. 2023).

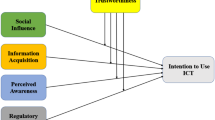

Understanding the elements that influence people’s attitudes toward adopting and integrating blockchain into accounting education is critical for successful implementation. Grani and Maranguni (2019) recognize TAM as a conceptual framework for comprehending individuals’ acceptance and adoption of new technologies. TAM posits that ease of use and perceived usefulness are primary determinants of users’ attitudes and intentions toward adopting a specific technology (Davis, 1989). The following subsections present the study’s hypotheses, illustrated in Fig. 1.

The study model comprises TAM and OS as a moderator.

Perceived ease of use (PEU)

Venkatesh and Bala (2008) define perceived ease of use (PEU) as an individual’s perception of how simple it is to use a particular technology without substantial effort. It captures the technology’s simplicity and user-friendliness. When individuals perceive a technology as easy to use, they tend to believe it would be beneficial for their tasks (Fathema et al. 2015). Many studies have found a positive relationship between PEU and perceived usefulness (PU) in the context of technology adoption. For instance, Venkatesh and Davis (2000) discovered a positive correlation between PEU and PU in their study on IT adoption within organizations. Similarly, Fathema et al. (2015) and Ullah et al. (2021) found a strong connection between PEU and PU in their research on IT adoption in education. This suggests that individuals are more likely to find technology advantageous when they consider it user-friendly.

Attitude (ATU) refers to individuals’ overall evaluation and inclination toward using a technology (Venkatesh et al. 2003). PEU plays a crucial role in shaping individuals’ attitudes by affecting their perception of how seamlessly they can adopt and integrate technology into their practices. Exploring technology integration in education sheds light on the relationship between PEU and ATU. For example, Teo (2011) investigated e-learning platform implementation in higher education and found a positive correlation between PEU and ATU. Likewise, Al-Hattami (2023) discovered that PEU significantly affects individuals’ ATU toward adopting technology in accounting education. These findings suggest that individuals who perceive technology as easy to use are more likely to have favorable attitudes toward incorporating it into their educational practices.

The literature generally suggests that PEU exerts a favorable influence on both PU and ATU in various contexts. This study presents its suppositions based on this evidence:

H1: PEU positively affects PU.

H2: PEU positively affects ATU.

Perceived usefulness (PU)

The concept of perceived usefulness (PU), as introduced by Davis (1989), refers to an individual’s belief that using a particular technology will enhance their job performance or productivity. Many studies have explored the relationship between PU and the adoption of emerging technologies, such as blockchain. Venkatesh and Davis (2000) investigated the factors that influence individuals’ intentions to adopt information technology. Their study found a significant positive correlation between PU and the adoption of new technologies, indicating that individuals are more likely to embrace technology when they perceive it as practically valuable. Additional research by Mukherjee et al. (2023) and Tasnim et al. (2023) explored the factors affecting the intention to adopt blockchain in supply chain management. Tasnim et al. (2023) discovered that PU had a significant positive impact on behavioral intention. Meanwhile, Mukherjee et al. (2023) found that PU had an indirect but positive effect on behavioral intention through attitude. A recent study by Al-Hattami (2023) examined the factors influencing the adoption of technology in accounting education. The findings showed that perceived usefulness was a significant determinant of attitude and adoption intention, supporting the idea that individuals are more likely to adopt blockchain in accounting education if they perceive it as useful. Based on the aforementioned references, the following hypotheses were formulated:

H3. PU positively affects ATU.

H4. PU positively affects the behavior intention of blockchain’s adoption and integration within accounting education.

Attitude (ATU)

The ATU is a key element of TAM and evaluates users’ overall perception of a technology. Research has explored the relationship between ATU and the behavioral intention to adopt various technologies, including blockchain (Fathema et al. 2015; Sciarelli et al. 2022; Al-Hattami, 2023; Mukherjee et al. 2023; Kumar et al. 2022; Kim et al. 2020). These studies consistently demonstrate a positive correlation between ATU and behavioral intention. For instance, Sciarelli et al. (2022) studied blockchain adoption among innovative Italian companies and found that a positive ATU significantly increased users’ intention to adopt blockchain in their work. Kumar et al. (2022) examined factors influencing blockchain adoption in higher education and discovered that a favorable attitude toward using blockchain technology positively impacted the behavioral intention to adopt it. Building on this foundation, the current research assesses the effect of ATU on the intention to adopt and integrate blockchain technology in accounting education.

H5. ATU positively influences the intention to adopt and integrate blockchain technology within accounting education.

Organizational support (OS)

OS is essential for promoting the acceptance and utilization of emerging technologies within institutions (Al-Hattami et al. 2024a, 2024b). In the context of technology integration in education, OS encompasses the resources, encouragement, and infrastructure provided by educational institutions to aid the adoption and integration process (Stone and Wang, 2009; Naujokaitiene et al. 2015). Various studies have underscored the positive influence of OS on individuals’ intentions to adopt and integrate new technologies. For instance, Larosiliere et al. (2016) discovered that the presence of OS fosters technology integration by creating a supportive environment that promotes its usage. Similarly, Huang et al. (2011) identified OS as a significant predictor when examining factors influencing teachers’ intentions to adopt educational technologies. In another context, Hussain et al. (2021) explored the factors affecting students’ intention to adopt e-banking technologies and found that OS significantly impacted their intention. Furthermore, Al-Hattami et al. (2024a, 2024b) studied the success of accounting systems at the organizational level and demonstrated that OS significantly affected the use of such systems in SMEs. Based on these findings, the current study proposes its sixth hypothesis:

H6. OS positively affects the behavior intention of blockchain’s adoption and integration within accounting education.

Besides potentially influencing behavioral intention directly, OS can also serve as a moderating factor. Research in specific contexts has already demonstrated this moderating effect (Hassan et al. 2019). Shaikh et al. (2023) noted that using “moderators” enables researchers to uncover new and interesting relationships. Despite the minimal focus on OS in the education field, there is limited research on the role of OS as a moderator in the relationship between factors influencing blockchain adoption and integration in accounting education (such as perceived usefulness and attitude toward use) and behavioral intention.

OS can moderate the relationship between perceived usefulness and behavioral intention toward blockchain adoption and integration in accounting education. The degree of OS provided can affect how educators perceive the usefulness of blockchain, thereby impacting their intention to adopt it. Additionally, OS may also moderate the connection between attitude toward use and behavioral intention in blockchain adoption in accounting education. The level of organizational support can shape educators’ perception and assessment of the technology, thus influencing their intention to adopt it. Based on this information, the following hypotheses are proposed:

H7. OS moderates the relationship between PU and behavior intention of blockchain’s adoption and integration within accounting education.

H8. OS moderates the relationship between ATU and behavior intention of blockchain’s adoption and integration within accounting education.

Methodology

The study design, sampling, and data collection

This research adopts a quantitative study design, employing a moderated model based on TAM. The study utilizes purposive sampling to focus on faculty members in Indian universities and colleges. This approach aims to accurately represent the specific population of interest, thereby enhancing the study’s relevance to the context under investigation (Hair et al. 2017; Creswell and Creswell, 2017).

The study used a structured questionnaire to collect quantitative insights. It included established constructs such as perceived usefulness, attitude, and organizational support. The use of a validated instrument ensures reliability and consistency in measurement (Venkatesh et al. 2003; Regmi et al. 2016; Al-Hattami et al. 2024a, 2024b). The questionnaire was distributed to the targeted sample via Google Docs and social media platforms such as WhatsApp, Messenger, and ResearchGate. Online surveys are a popular method of data collection due to the growing prevalence of internet use and the decreasing cost of technological devices. This approach offers an economical and efficient means of data gathering within a short timeframe (Regmi et al. 2016). Additionally, this method is suitable and safe, particularly given the challenges of epidemics such as COVID-19 (Al-Hattami et al. 2023; Al-Hattami and Almaqtari, 2023).

The questionnaire comprised two main sections. The first section asked faculty members for personal details such as age, gender, and qualifications. Among the respondents, 111 were male and 77 were female, representing 59.04 and 40.96% of the total sample, respectively. In terms of age groups, there were 23 respondents under 30, 82 aged 30–40, and 83 over 40, corresponding to 12.23, 43.62, and 44.15% of the total sample, respectively. Respondents’ educational qualifications were categorized as doctorate, postgraduate, and other. Of the respondents, 146 held a doctorate, 38 had a postgraduate degree, and 4 had qualifications in the “other” category. These categories made up 77.66%, 20.21%, and 2.13% of the sample, respectively.

Respondents’ positions in the academic hierarchy were categorized as teaching assistant, assistant professor, associate professor, and professor. There were 36 teaching assistants, 70 assistant professors, 49 associate professors, and 33 professors, constituting 19.15%, 37.23%, 26.06%, and 17.55% of the sample, respectively. The respondents’ levels of expertise were determined by their years of teaching experience and were categorized as follows: less than 2 years, 2–5 years, 6–10 years, 11–15 years, and more than 15 years.

Table 1 details the number of respondents in each expertise category and their corresponding percentages. Table 2 outlines the second section, which assessed TAM’s PU and ATU with four items and PEU with three items (Davis, 1989; Fathema et al. 2015; Alshurafat et al. 2021; Al-Hattami, 2023). It also measured BIB with three items (Smith, 2017; Tasnim et al. 2023; Al-Hattami, 2023) and OS with four items (Huang et al. 2011; Li et al. 2022).

After distributing the survey link, 191 valid responses were received. Although the sample size of 191 faculty members may appear small, the use of advanced statistical methods such as SmartPLS 4 software supports the reliability of the results (Hair et al. 2017).

Common method bias (CMB)

The study acknowledges the potential for CMB and aims to minimize it by meticulously designing the questionnaire and ensuring respondents’ anonymity. Additionally, the study employed statistical techniques, including the variance inflation factor (VIF) test, to assess CMB (Kock, 2015). Despite considering non-response bias, the study aimed to mitigate its impact by promoting clear communication, providing reminders, and emphasizing the significance of each respondent’s input.

A Statistical tool used

SmartPLS 4 was used to analyze the valid responses. This widely-used software offers a user-friendly interface that simplifies the process of building and analyzing complex models. It provides advanced analytical capabilities and requires less technical expertise compared to other SEM software like AMOS or CB-SEM, making it a popular choice among researchers in various fields, including technology acceptance in education (Henseler et al. 2016; Alshurafat et al. 2021; Al-Hattami, 2023). Researchers also favor SmartPLS over regression analysis for evaluating moderation (Gefen et al. 2000; Almaqtari et al. 2023). Additionally, it is a suitable technique for small sample sizes and non-normal data (Afthanorhan, 2013; Chin, 1998). SmartPLS facilitates both measurement model estimation and structural model estimation, enabling the examination of relationships between latent variables. It offers robust statistical methods for assessing model fit, the validity of measurement scales, and the reliability of constructs. Furthermore, it employs bootstrapping techniques to assess the statistical significance of path coefficients and indirect effects (Henseler et al. 2016; Hair et al. 2019).

Data analysis and results

To conduct the analysis using SmartPLS, the researcher can follow these two steps: a) assess the measurement model by evaluating the validity and reliability of the latent constructs (Hair et al. 2019). Common reliability measures include Cronbach’s alpha (C-A) and composite reliability (C-R). C-A evaluates the average inter-item correlation within a construct, while C-R assesses the shared variance among its indicators. Both should be at least 0.70 (Hair et al. 2019). This study established reliability as all constructs’ C-A and C-R values exceeded 0.70 (Table 3). Validity ensures the measurement items accurately represent the intended construct. Researchers typically assess convergent validity (C-V) and discriminant validity (D-V). Examining each construct’s average variance extracted (AVE) serves to evaluate convergent validity. According to Fornell and Larcker (1981), AVE should be above 0.5, indicating that the construct accounts for at least 50% of the variance in the indicators. Discriminant validity is determined by comparing each construct’s AVE to the intercorrelations among constructs (Hair et al. 2019). This study achieved C-V and D-V because the AVE exceeded 0.5 and the correlation values for each construct were lower than the AVE (Table 3).

It is important to consider multicollinearity and CMB in the measurement model, as they are undesirable factors (Hair et al. 2017). The most common method for assessing these issues is VIF. According to Hair et al. (2017) and Kock (2015), a VIF value should not exceed 5 to suggest the absence of multicollinearity and should not exceed 3.3 to suggest the absence of CMB. Table 3 shows that the maximum VIF score is 3.253, indicating there are no significant multicollinearity or CMB issues.

b) Following the examination of the measurement model, the study proceeded to estimate the structural model to assess the relationships between latent constructs and test the hypotheses. This step involves analyzing the connections between latent variables such as PU and ATU and the dependent variable, which is BIB. SmartPLS computes path coefficients, also known as t-values, and applies the recommended threshold values. A t-value greater than 1.96 (at a significance level of 0.05) typically suggests statistical significance (Hair et al. 2011). Additionally, SmartPLS provides statistical measures to evaluate model fit, including the R-squared value (representing the variance explained by the model) and predictive relevance (Q²). These metrics help assess the overall quality and predictive capability of the structural model (Falk and Miller, 1992; Hair et al. 2011).

The study confirmed all the proposed hypotheses with varying levels of significance (Table 4). The bootstrapping analysis, which involved 5000 subsamples, provided evidence supporting hypothesis H1 (t = 9.612; Beta = 0.589; p < 0.001). The results also supported hypotheses H2 (t = 4.762; Beta = 0.357; p < 0.001), H3 (t = 7.920; Beta = 0.565; p < 0.001), H4 (t = 2.308; Beta = 0.223; p < 0.05), H5 (t = 4.825; Beta = 0.366; p < 0.001), H6 (t = 3.023; Beta = 0.215; p < 0.01), H7 (t = 2.971; Beta = 0.171; p < 0.01), and H8 (t = 2.222; Beta = 0.130; p < 0.05).

The R-squared value, which ranges from zero to one, measures the model’s predictive accuracy. A higher R-squared value signifies a more accurate prediction, with a value above 0.10 typically deemed satisfactory and significant (Falk and Miller, 1992). In this study, PU, ATU, and OS (Fig. 2; Table 4) explained approximately 64% of the variance in “BIB.” To assess Q², the Stone-Geisser approach was employed using blindfolding techniques. A Q² value above zero is considered acceptable (Hair et al. 2011). As shown in Table 5, the Q² scores are above zero, confirming the predictive significance of the research model.

This fig. displays the results of data analysis.

Discussion

In the discussion section, the study delves into the pivotal role of the ease of integrating blockchain into existing accounting curricula, perceived usefulness, attitude, and organizational support as critical factors influencing BIB. Building on these factors, the results show that faculty members who perceive blockchain technology as comprehensible, easy to implement, and easy to teach are more likely to embrace its incorporation into their classrooms. This, in turn, reinforces their positive attitudes and recognition of the benefits of integrating blockchain into accounting education (supporting H1 and H2). Al-Hattami (2023), Fathema et al. (2015), and Teo (2011) conducted previous research that aligns with these findings, providing additional support and context for the current study. These scholars have previously explored aspects related to technology adoption and integration within educational settings, offering insights that resonate with these research outcomes. Al-Hattami (2023) contributes valuable insights into the technological adoption landscape by highlighting the importance of educators’ perceptions and ease of use. Similarly, Fathema et al. (2015) shed light on the significance of user-friendly interfaces in educational technology, emphasizing the role of usability in enhancing the overall learning experience. In this study, the resonance with these earlier works underscores the universality of the challenges and opportunities associated with technological integration in educational contexts. The positive correlation between faculty members’ ease of comprehension, implementation, and teaching of blockchain technology and their willingness to adopt it mirrors the findings of these past studies, emphasizing the enduring nature of these factors across different technological landscapes.

The results emphasize the importance of PU in shaping educators’ attitudes and intentions toward incorporating blockchain technology in accounting education. Prior research, such as studies by Kshetri (2018), Smith (2017), Chen et al. (2018), and Quinto (2022), has recognized the key role of PU. The current study reveals that faculty members who view blockchain as beneficial for teaching essential accounting concepts are more likely to integrate it into the curriculum. These findings support existing literature, suggesting that PU significantly influences attitudes toward usage and behavioral intention (H3 and H4). Additionally, this study aligns with earlier research by Venkatesh and Davis (2000), Al-Hattami (2023), and Mukherjee et al. (2023), which confirmed the link between PU and behavioral intention. The current study reinforces this relationship by contributing to the growing body of evidence that PU plays a crucial role in shaping educators’ intentions to adopt new technologies like blockchain in academic environments.

Lastly, the study underscores the crucial role of organizational support in influencing faculty members’ BIB. Consistent with prior studies by Nokiti and Yusof (2019) and Stone and Wang (2009), the findings highlight that organizational support significantly enhances educators’ perceptions of the value and usefulness of blockchain technology. When faculty members feel supported by their university, they are more likely to perceive blockchain adoption as beneficial and necessary, thereby increasing their intention to adopt and integrate it into the curriculum.

In recent years, the significance of organizational support (OS) has emerged as a critical factor influencing the successful implementation of innovative technologies within educational settings. Mohammad and Vargas (2022) emphasized OS’s critical role in addressing challenges associated with the use of blockchain technology in education. Building on this foundation, it becomes imperative to delve deeper into the nuanced ways in which OS acts as a moderator in the context of blockchain integration in accounting education.

Existing literature provides ample evidence to support the assertion that OS can effectively mitigate perceived barriers to technology adoption. According to Mohammad and Vargas (2022), educational institutions can alleviate concerns about the complexity and costs of blockchain integration by providing comprehensive support mechanisms. This includes, among other things, the provision of training programs, technical assistance, and the allocation of financial resources. Stone and Wang (2009) also affirm this notion, highlighting how OS can foster a conducive environment for technology adoption within academic institutions.

The moderating effects of OS (H7 and H8) underscore a crucial dimension of its influence on the relationship between various constructs. Specifically, educational institutions’ level of support determines the positive associations between PU and BIB, as well as between ATU and BIB. In essence, increased OS serves to amplify faculty members’ positive attitudes and intentions toward the adoption and integration of blockchain technology in accounting education.

Moreover, it is imperative to recognize that organizational support extends beyond the mere provision of resources; it encompasses a broader culture of encouragement and advocacy for technological innovation. When educational institutions actively endorse and champion the integration of blockchain technology, faculty members are not only more likely to perceive its value but also exhibit a heightened willingness to embrace it as a pedagogical tool. This underscores the symbiotic relationship between organizational support and the successful implementation of transformative technologies within educational contexts.

In light of these insights, it becomes evident that fostering a robust culture of organizational support is paramount for realizing the full potential of blockchain technology in accounting education. Educational institutions can foster an environment where faculty members can embrace innovative teaching and learning by prioritizing initiatives that promote training, assistance, and resource allocation. Thus, investing in organizational support emerges as a strategic imperative for educational institutions seeking to harness the transformative power of blockchain technology in the realm of accounting education.

Conclusion

In conclusion, the application of TAM to the realm of blockchain adoption within accounting education underscores the pivotal role of various factors in shaping faculty members’ intentions to incorporate blockchain into their curriculum. Building upon prior research, this study reaffirms the significance of perceived usefulness, perceived ease of use, attitude, and organizational support as critical drivers influencing the adoption and integration of blockchain technology.

The findings of this research underscore the importance of faculty members’ perceptions regarding the value and utility of blockchain technology. When faculty members perceive blockchain as beneficial and advantageous for accounting education, they are more likely to incorporate it into their teaching practices. Moreover, the perceived ease of use of blockchain tools and platforms plays a crucial role in facilitating their adoption among accounting educators. Faculty members are more likely to embrace blockchain integration when they perceive it as user-friendly and accessible. Furthermore, accounting faculty members’ attitudes towards blockchain emerge as a significant determinant of its adoption in accounting education. A positive attitude towards blockchain technology fosters a favorable environment for its integration into the curriculum, encouraging experimentation and exploration of its potential applications in accounting pedagogy. Furthermore, adequate organizational support emerges as a key enabler for facilitating the successful adoption and integration of blockchain in accounting education. Educational institutions and policymakers need to recognize the importance of providing resources, training, and institutional support to empower faculty members to effectively incorporate blockchain technology into their teaching practices.

By comprehensively understanding these determinants, educational institutions and policymakers can devise targeted strategies and initiatives to promote the widespread adoption and integration of blockchain within accounting education. Through proactive measures aimed at enhancing perceived usefulness, ease of use, fostering positive attitudes, and providing organizational support, stakeholders can harness the transformative potential of blockchain technology to enrich accounting education and equip future professionals with essential skills and knowledge for the evolving digital landscape.

Implications

The adoption of blockchain technology in accounting education represents a burgeoning area of study with significant managerial and social implications. Previous research has identified various factors influencing the intention to adopt blockchain within educational contexts, yet there remains ample room for exploration, particularly within the Indian context. This study fills this gap by introducing a conceptual model based on TAM, which sheds light on the factors that influence blockchain adoption and integration in accounting education.

From a managerial perspective, grasping elements such as PU, PEU, and OS is essential for successfully incorporating blockchain technology into accounting education. Educational institutions must acknowledge blockchain’s potential to improve learning outcomes and better prepare students for the complexities of modern accounting practices. Faculty members, who play a central role in technology integration, need support and training to encourage positive attitudes toward blockchain adoption. Institutions should implement policies to support faculty development programs, providing resources such as training sessions, workshops, and seminars to equip educators with the knowledge and skills necessary to effectively integrate blockchain into their teaching methods.

Socially, the integration of blockchain in accounting education carries profound implications for the future of the profession and broader society. By embracing blockchain technology, educational institutions can empower students with the skills needed to navigate a rapidly evolving financial landscape. This not only enhances individual career prospects but also contributes to the overall resilience and efficiency of financial systems. Additionally, by fostering a culture of innovation and technology adoption within academia, institutions can play a pivotal role in shaping societal attitudes towards emerging technologies like blockchain, driving broader adoption, and fostering digital literacy among future generations.

In summary, this study underscores the importance of considering managerial and social implications when integrating blockchain into accounting education. By addressing key factors influencing adoption and providing support to faculty members, institutions can harness the transformative potential of blockchain technology, shaping both the future of the accounting profession and broader societal perceptions of emerging technologies.

Limitations

When interpreting the results of this study, it is essential to consider several limitations. First, the limited sample size may limit the generalizability of the findings. While the insights provided are valuable within the study’s specific context, they may not apply to broader or different contexts. Secondly, conducting the research in India could potentially introduce geographical bias. Future research should include participants from diverse countries to capture variations in adoption patterns, cultural influences, and regulatory frameworks. Third, the study focused exclusively on TAM theory. Expanding future studies to include other adoption theories could provide a broader perspective. Fourth, the COVID-19 pandemic impacted the ability to conduct in-person interviews, which could have offered a more in-depth evaluation. Furthermore, the study did not examine the impact of demographic factors such as expertise and education level, as well as other moderators like social influence. Further research should explore the significance of these variables in the acceptance of blockchain in accounting education.

The study’s OS-related questions may not fully represent the broader range of factors influencing faculty engagement and satisfaction. The study’s objectives align with the questions, but they may overlook other aspects of OS, potentially leading to an incomplete understanding of its role. Additionally, using teaching assistants introduces another limitation. Although teaching assistants provide valuable support and increase educational efficiency, their involvement can lead to variability in educational content delivery and assessments. This variability might affect the consistency and generalizability of the findings, especially if teaching assistants have different experience levels or teaching styles. These limitations could influence the methodology’s assumptions and conclusions. For instance, the impact of OS and teaching assistants on outcomes might be more complex than the analysis captures. The study may not fully explore how these factors interact with other variables. Recognizing these limitations is important for interpreting the findings, and future research should explore a broader range of OS-related factors and standardize teaching assistant involvement. Addressing these limitations and conducting further research in this area can provide a more robust understanding of blockchain adoption and integration within accounting education. The results should be viewed with these limitations in mind.

Data availability

Due to privacy concerns, the data supporting the findings of this study are not publicly available. Although the data was collected using the anonymous identity of the respondent, the author has promised confidentiality to his participants. Therefore, sharing the data would violate this commitment. Researchers who wish to access the data to verify the findings or conduct further research may contact the corresponding author.

References

Afthanorhan WMABW (2013) A comparison of partial least square structural equation modeling (PLS-SEM) and covariance based structural equation modeling (CB-SEM) for confirmatory factor analysis. International Journal of Engineering Science and Innovative Technology 2(5):198–205

Al-Adwan AS, Li N, Al-Adwan A, Abbasi GA, Albelbis NA, Habibi A (2023) Extending the Technology Acceptance Model (TAM) to Predict University Students’ Intentions to Use Metaverse-Based Learning Platforms. Education and Information Technologies, 1–33

Albayati H, Kim SK, Rho JJ (2020) Accepting financial transactions using blockchain technology and cryptocurrency: a customer perspective approach. Technology in Society 62:101320

Al-Hattami HM (2021) University accounting curriculum, IT, and job market demands: evidence from Yemen. Sage Open 11(2):1–14. https://doi.org/10.1177/21582440211007111

Al-Hattami HM (2023) Understanding perceptions of academics toward technology acceptance in accounting education. Heliyon 9(1):e13141. https://doi.org/10.1016/j.heliyon.2023.e13141

Al-Hattami HM, Almaqtari FA (2023) What determines digital accounting systems’ continuance intention? An empirical investigation in SMEs. Humanities and Social Sciences Communications 10(1):1–13

Al-Hattami HM, Al-Adwan AS, Abdullah AAH, Al-Hakimi MA (2023) Determinants of customer loyalty toward mobile wallet services in post-COVID-19: the moderating role of trust. Human Behavior and Emerging Technologies 2023:9984246. https://doi.org/10.1155/2023/9984246. 13 pages, 2023

Al‐Hattami HM, Almaqtari FA, Abdullah AAH, Al‐Adwan AS (2024a) Digital accounting system and its effect on corporate governance: an empirical investigation. Strategic Change 33(3):151–167

Al-Hattami HM, Senan NAM, Al-Hakimi MA, Azharuddin S (2024b) An empirical examination of AIS success at the organizational level in the era of COVID-19 pandemic. Global Knowledge, Memory and Communication 73(3):312–330

Almaqtari FA, Farhan NH, Al-Hattami HM, Elsheikh T (2023) The moderating role of information technology governance in the relationship between board characteristics and continuity management during the Covid-19 pandemic in an emerging economy. Humanities and Social Sciences Communications 10(1):1–16

AlShamsi M, Al-Emran M, Shaalan K (2022) A systematic review on blockchain adoption. Applied Sciences 12(9):4245

Alshurafat H, Al Shbail MO, Masadeh WM, Dahmash F, Al-Msiedeen JM (2021) Factors affecting online accounting education during the COVID-19 pandemic: An integrated perspective of social capital theory, the theory of reasoned action and the technology acceptance model. Education and Information Technologies 26(6):6995–7013

Al-Rahmi A. M, Al-Rahmi W. M, Alturki U, Aldraiweesh A, Almutairy S, Al-Adwan A. S (2022) Acceptance of mobile technologies and M-learning by university students: An empirical investigation in higher education. Education and Information Technologies 27(6):7805–7826

Al-Swidi AK, Al-Hakimi MA, Al Halbusi H, Al Harbi JA, Al-Hattami HM (2024) Does blockchain technology matter for supply chain resilience in dynamic environments? The role of supply chain integration. Plos one 19(1):e0295452

Bagozzi RP, Yi Y (1988) On the evaluation of structural equation models. Journal of the academy of marketing science 16:74–94

Bhaskar P, Tiwari CK, Joshi A (2021) Blockchain in education management: present and future applications. Interactive Technology and Smart Education 18(1):1–17

Bonsón E, Bednárová M (2019) Blockchain and its implications for accounting and auditing. Meditari Accountancy Research 27(5):725–740

Chen G, Xu B, Lu M, Chen NS (2018) Exploring blockchain technology and its potential applications for education. Smart Learning Environments 5(1):1–10

Chin WW (1998) The partial least squares approach to structural equation modeling. Modern methods for business research 295(2):295–336

Creswell JW, Creswell JD (2017) Research design: Qualitative, quantitative, and mixed methods approaches

Dash MK, Panda G, Kumar A, Luthra S (2022) Applications of blockchain in government education sector: a comprehensive review and future research potentials. Journal of Global Operations and Strategic Sourcing 15(3):449–472

Davis FD (1989) Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly 13(3):319–340

Dehghani M, Kennedy RW, Mashatan A, Rese A, Karavidas D (2022) High interest, low adoption. A mixed-method investigation into the factors influencing organisational adoption of blockchain technology. Journal of Business Research 149:393–411

Falk RF, Miller NB (1992) A primer for soft modeling. University of Akron Press

Fathema N, Shannon D, Ross M (2015) Expanding the Technology Acceptance Model (TAM) to examine faculty use of Learning Management Systems (LMSs) in higher education institutions. Journal of Online Learning & Teaching 11(2):210–233

Fernandez D, Guat LP (2023) Model of Blockchain Technology in Malaysian Accounting Education Learning Context: A Theoretical Paper. Malaysian Journal of Social Sciences and Humanities (MJSSH) 8(11):e002625–e002625

Fornell C, Larcker DF(1981) Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18(1):39–50

Gado S, Kempen R, Lingelbach K, Bipp T (2022) Artificial intelligence in psychology: How can we enable psychology students to accept and use artificial intelligence? Psychology Learning & Teaching 21(1):37–56

Gefen D, Straub D, Boudreau MC (2000) Structural equation modeling and regression: Guidelines for research practice. Communications of the association for information systems 4(1):1–77

Granić A, Marangunić N (2019) Technology acceptance model in educational context: A systematic literature review. British Journal of Educational Technology 50(5):2572–2593

Habib G, Sharma S, Ibrahim S, Ahmad I, Qureshi S, Ishfaq M (2022) Blockchain Technology: Benefits, Challenges, Applications, and Integration of Blockchain Technology with Cloud Computing. Future Internet 14(11):341

Hair JF, Ringle CM, Sarstedt M (2011) PLS-SEM: Indeed a silver bullet. Journal of Marketing theory and Practice 19(2):139–152

Hair JF, Risher JJ, Sarstedt M, Ringle CM (2019) When to use and how to report the results of PLS-SEM. European business review 31(1):2–24

Hair Jr JF, Hult GTM, Ringle C, Sarstedt M (2017) A Primer on Partial Least SquaresStructural Equation Modeling (PLS-SEM), Second Edition. Sage publications

Hassan N, Yaakob SA, Sumardi NA, Mat Halif M, Ali S, Abdul Aziz R, Abdul Majid A (2019) The Moderating Effects of Perceived Organizational Support on the Relationship Between Technostress Creators and Organizational Commitment Among School Teachers. International Journal of Engineering and Advanced Technology (IJEAT) 8(3S):206–210

Henseler J, Hubona G, Ray PA (2016) Using PLS path modeling in new technology research: updated guidelines. Industrial management & data systems 116(1):2–20. https://doi.org/10.1108/IMDS-09-2015-0382

Huang RT, Deggs DM, Jabor MK, Machtmes K (2011) Faculty online technology adoption: The role of management support and organizational climate. Online Journal of Distance Learning Administration 14(2):1–11

Hussain A, Hussain MS, Marri MYK, Zafar MA (2021) Acceptance of Electronic Banking among University Students in Pakistan: An Application of Technology Acceptance Model (TAM). Pakistan Journal of Humanities and Social Sciences 9(2):101–113

ICAEW (2018) Blockchain and the future of accountancy. Retrieved from https://www.icaew.com/-/media/corporate/files/technical/technology/thought-leadership/blockchain-and-the-future-of-accountancy.ashx (Accessed May 5, 2023)

Javaid M, Haleem A, Singh RP, Suman R, Khan S (2022) A review of Blockchain Technology applications for financial services. BenchCouncil Transactions on Benchmarks, Standards and Evaluations 2(3):100073. https://doi.org/10.1016/j.tbench.2022.100073

Kim J, Merrill K, Xu K, Sellnow DD (2020) My teacher is a machine: Understanding students’ perceptions of AI teaching assistants in online education. International Journal of Human–Computer Interaction 36(20):1902–1911

Kock N (2015) Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration (ijec) 11(4):1–10

Kroon N, Alves MDC (2023) Fifteen years of accounting professional’s competencies supply and demand: Evidencing actors, competency assessment strategies, and ‘top three’competencies. Administrative Sciences 13(3):70

Kshetri N (2018) 1 Blockchain’s roles in meeting key supply chain management objectives. International Journal of Information Management 39:80–89

Kumar N, Singh M, Upreti K, Mohan D (2022) Blockchain adoption intention in higher education: role of trust, perceived security and privacy in technology adoption model. In Proceedings of International Conference on Emerging Technologies and Intelligent Systems: ICETIS 2021 (Volume 1) (pp. 303–313)

Larosiliere GD, McHaney R, Kobelsky K (2016) The effects of IT management on technology process integration. Journal of Computer Information Systems 56(4):341–351

Li C, Zhang Y, Xu Y (2022) Factors Influencing the Adoption of Blockchain in the Construction Industry: A Hybrid Approach Using PLS-SEM and fsQCA. Buildings 12(9):1349

Lin Y, Yu Z (2023) Extending Technology Acceptance Model to higher-education students’ use of digital academic reading tools on computers. International Journal of Educational Technology in Higher Education 20(1):34

Mohammad A, Vargas S (2022) Challenges of Using Blockchain in the Education Sector: A Literature Review. Applied Sciences 12(13):6380

Moore WB, Felo A (2022) The evolution of accounting technology education: Analytics to STEM. Journal of Education for Business 97(2):105–111

Mukherjee S, Baral MM, Lavanya BL, Nagariya R, Singh Patel B, Chittipaka V (2023) Intentions to adopt the blockchain: investigation of the retail supply chain. Management Decision 61(5):1320–1351. https://doi.org/10.1108/MD-03-2022-0369

Naujokaitiene J, Tereseviciene M, Zydziunaite V (2015) Organizational support for employee engagement in technology-enhanced learning. Sage Open 5(4):2158244015607585

Nokiti AE, Yusof SAM (2019) Exploring the Perceptions of Applying Blockchain Technology in the Higher Education Institutes in the UAE. Multidisciplinary Digital Publishing Institute Proceedings 28(1)):8

Novak A, Barišić I, Žager K (2022, September) Implications of Blockchain Application to Accounting Education and Accounting Practice. In ECIE 2022 17th European Conference on Innovation and Entrepreneurship. Academic Conferences and publishing limited

Polimeni RS, Burke JA (2021) Integrating emerging accounting digital technologies and analytics into an undergraduate accounting curriculum—A case study. Journal of Emerging Technologies in Accounting 18(1):159–173

PWC (2018) Blockchain Is Here. What’s Your next Move? PwC’s Global Blockchain Survey 2018. https://www.pwc.com/jg/en/publications/blockchain-is-here-next-move.html

Qasim A, Kharbat FF (2020) Blockchain technology, business data analytics, and artificial intelligence: Use in the accounting profession and ideas for inclusion into the accounting curriculum. Journal of emerging technologies in accounting 17(1):107–117

Quinto II, EJ (2022) How Technology Has Changed the Field of Accounting. In BSU Honors Program Theses and Projects. Item 558. Available at: https://vc.bridgew.edu/honors_proj/558

Regmi PR, Waithaka E, Paudyal A, Simkhada P, van Teijlingen E (2016) Guide to the design and application of online questionnaire surveys. Nepal journal of epidemiology 6(4):640–644

Sarwar MI, Iqbal MW, Alyas T, Namoun A, Alrehaili A, Tufail A, Tabassum N (2021) Data vaults for blockchain-empowered accounting information systems. IEEE Access 9:117306–117324

Savelyeva T, Park J (2022) Blockchain technology for sustainable education. British Journal of Educational Technology 53(6):1591–1604

Sciarelli M, Prisco A, Gheith MH, Muto V (2022) Factors affecting the adoption of blockchain technology in innovative Italian companies: an extended TAM approach. Journal of Strategy and Management 15(3):495–507

Shaikh AA, Alamoudi H, Alharthi M, Glavee-Geo R (2023) Advances in mobile financial services: a review of the literature and future research directions. International Journal of Bank Marketing 41(1):1–33. https://doi.org/10.1108/IJBM-06-2021-0230

Singh M, Joshi M, Sharma S (2023) Integrating Blockchain Technology into Accounting Curricula: A Template for Accounting Educators. In Handbook of Big Data and Analytics in Accounting and Auditing (pp. 337–360). Singapore: Springer Nature Singapore

Sledgianowski D, Gomaa M, Tan C (2017) Toward integration of Big Data, technology and information systems competencies into the accounting curriculum. Journal of Accounting Education 38:81–93

Smith SS (2017) Integrating blockchain and artificial intelligence into the accounting curriculum. Journal of Accountancy, Newsletter. Retrieved from https://www.journalofaccountancy.com/newsletters/extra-credit/blockchain-artificial-intelligence-accounting-curriculum.html (Accessed May 6, 2023)

Stern M, Reinstein A (2021) A blockchain course for accounting and other business students. Journal of Accounting Education 56:100742

Stone DE, Wang CX (2009) Organizational Support for the Adoption of Educational Technology Association for Educational Communications and Technology 1:443–447. http://members.aect.org/pdf/Proceedings/proceedings09/2009/09_54. pdf Retrieved from

Tasnim Z, Shareef MA, Baabdullah AM, Hamid ABA, Dwivedi YK (2023) An Empirical Study on Factors Impacting the Adoption of Digital Technologies in Supply Chain Management and What Blockchain Technology Could Do for the Manufacturing Sector of Bangladesh. Information Systems Management, 1-23. https://doi.org/10.1080/10580530.2023.2172487

Teo T (2011) Factors influencing teachers’ intention to use technology: Model development and test. Computers & Education 57(4):2432–2440

Trapnell JE (2023) Accounting Education Disrupted: Transforming to Face a Challenging Future. The CPA Journal. Retrieved from: https://www.cpajournal.com/2023/12/29/accounting-education-disrupted/

Ullah N, Mugahed Al-Rahmi W, Alzahrani AI, Alfarraj O, Alblehai FM (2021) Blockchain technology adoption in smart learning environments. Sustainability 13(4):1801

Venkatesh V, Bala H (2008) Technology acceptance model 3 and a research agenda on interventions. Decision sciences 39(2):273–315

Venkatesh V, Davis FD (2000) A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science 46(2):186–204

Venkatesh V, Morris MG, Davis GB, Davis FD (2003) User Acceptance of Information Technology: Toward a Unified View. MIS Quarterly 27(3):425–478

Funding

This research received no external funding.

Author information

Authors and Affiliations

Contributions

The author conceived and designed the research; Performed the study; Analyzed and interpreted the data; Contributed reagents, materials, analysis tools or data; Wrote the paper.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors.

Informed consent

Consent was not deemed necessary for this study, as the data collected using the anonymous identity of the respondent. All sources used in this study have been considered and cited.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Al-Hattami, H.M. What factors influence the intention to adopt blockchain technology in accounting education?. Humanit Soc Sci Commun 11, 787 (2024). https://doi.org/10.1057/s41599-024-03315-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-03315-8